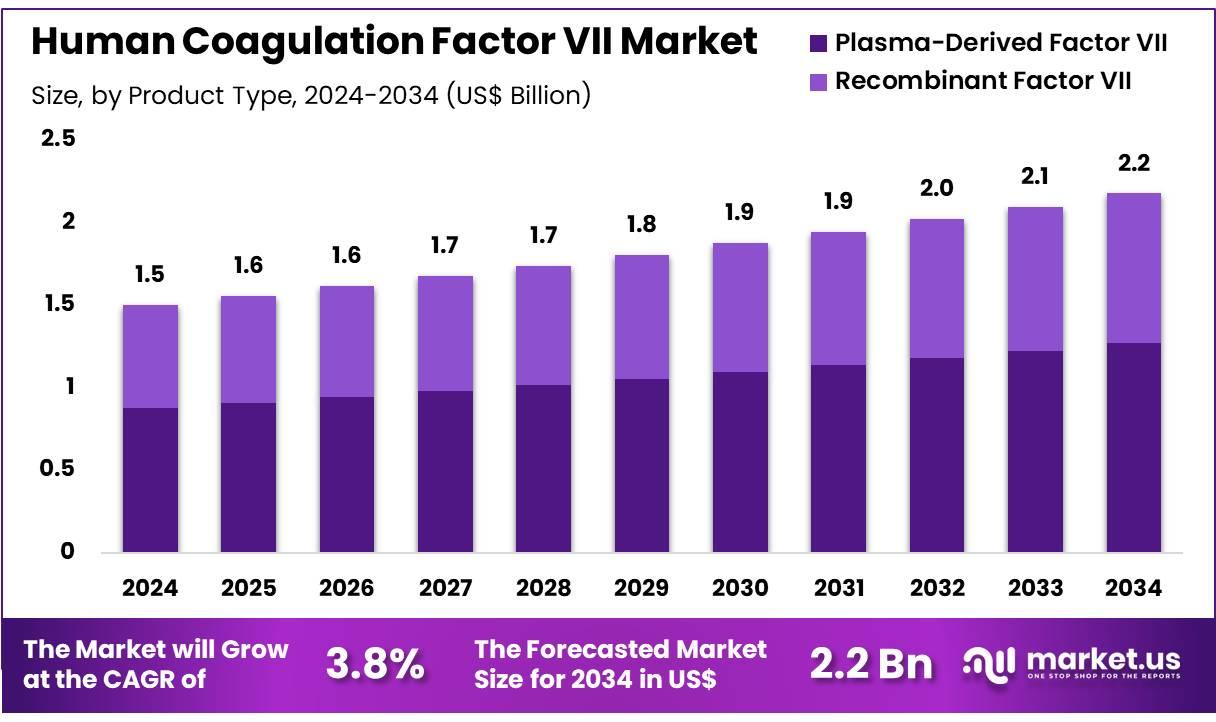

The Global Human Coagulation Factor VII market is projected to reach approximately USD 2.2 billion by 2034, rising from USD 1.5 billion in 2024. This indicates a steady CAGR of 3.8% from 2025 to 2034. North America held the dominant position in 2024, accounting for more than 38.2% of global revenue, or around USD 0.6 billion. This market is witnessing growth due to increased investment in bleeding disorder therapies and a strong presence of healthcare infrastructure in the region.

Ongoing research in gene therapy is a major driver for innovation in this market. While gene therapies for hemophilia A and B, such as Roctavian and Hemgenix, focus on Factor VIII and IX deficiencies, they influence the broader bleeding disorder landscape. These developments create momentum for improving current therapies, including Factor VII. The research is helping companies gain insights that can be applied to bypassing agents like recombinant Factor VII, enhancing their safety and efficacy profiles.

Companies are actively working on next generation Factor VIIa formulations. These products aim to offer better pharmacokinetics, enabling fewer injections and improved bleed control. Additionally, there is growing attention on personalized therapies for patients with inhibitors, where Factor VII plays a key role. This focus on tailored treatment is driving further advancement in both recombinant and plasma derived formulations, ensuring patients receive optimized care based on their clinical needs.

Despite progress in gene therapy, significant challenges remain in terms of cost, accessibility, and long term outcomes. These gaps open up opportunities for traditional treatments to evolve. As regulatory bodies like the U.S. FDA continue to approve new therapies, the entire treatment ecosystem is evolving. This shifting environment encourages continuous refinement of existing Factor VII products, positioning the market for sustained growth through a mix of conventional and cutting edge solutions.