Global Mobile Artificial Intelligence Market Anticipated to Expand Rapidly From 2025 to 2029

Use Code ONLINE20 to Save 20% On Global Market Reports – Gain Access to Trusted Market Data, Growth Indicators, and Industry Analytics

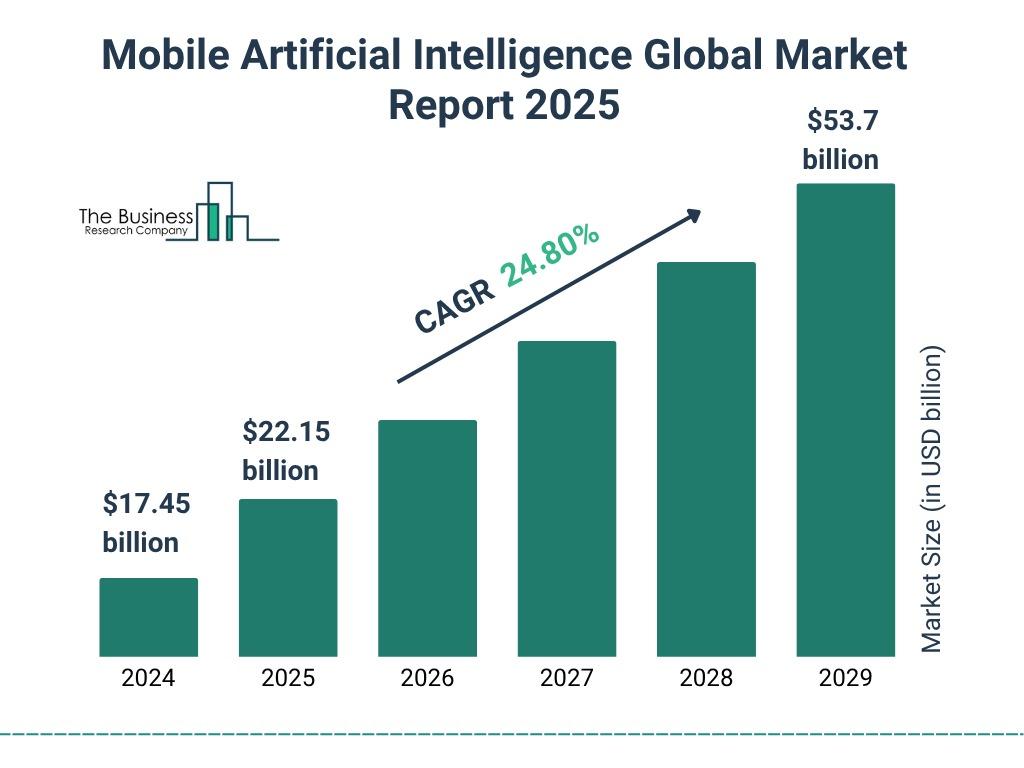

What Is the Current Size and Annual Growth Rate of the Mobile Artificial Intelligence Market?

The mobile artificial intelligence market size has grown exponentially in recent years. It will grow from $17.45 billion in 2024 to $22.15 billion in 2025 at a compound annual growth rate (CAGR) of 26.9%. The growth in the historic period can be attributed to growing adoption of smartphones and tablets, increasing research and development activities, increasing awareness of the ai-based solutions, growing dependency on iot devices.

The mobile artificial intelligence market size is expected to see exponential growth in the next few years. It will grow to $53.7 billion in 2029 at a compound annual growth rate (CAGR) of 24.8%. The growth in the forecast period can be attributed to increasing adoption of ai-based solutions across various industries, increasing power of mobile processors, development of new mobile ai software frameworks, growing demand for mobile ai applications. Major trends in the forecast period include ai chipsets, advancements in hardware, ai-powered mobile apps, edge ai, 5g connectivity.

Get your free report sample today:

Mobile Artificial Intelligence Market Forecast And Analysis Sample (https://www.thebusinessresearchcompany.com/sample.aspx?id=12875&type=smp)

What Are the Primary Factors Driving the Mobile Artificial Intelligence Market?

The increasing penetration of smartphones is expected to propel the growth of the mobile artificial intelligence market going forward. Smartphones are handheld electronic devices that combine the functionalities of a mobile phone and a personal computer. Smartphones play a significant role in implementing and using mobile artificial intelligence (AI) and serve as powerful and versatile platforms for mobile AI, enabling AI-driven functionalities, personalized experiences, intelligent interactions and on-the-go AI processing. For instance, in February 2023, according to Uswitch Limited, a UK-based price comparison and switching service company, there were 71.8 million mobile connections in the UK, a 3.8% (or around 2.6 million) increase over 2021. The UK population is expected to grow to 68.3 million by 2025, of which 95% (or about 65 million individuals) will own a smartphone. Therefore, the increasing penetration of smartphones will drive the growth of the mobile artificial intelligence market.

How Is the Mobile Artificial Intelligence Market Categorized Based on Key Segments?

The mobile artificial intelligencemarket covered in this report is segmented –

1) By Component: Hardware, Software, Services

2) By Technology Node: 20–28 Nano Meter (NM), 10 Nano Meter (NM), 7 Nano Meter (NM), Other Technology Nodes

3) By Application: Smartphones, Robotics, Augmented Reality (AR) And Virtual Reality(VR), Cameras, Drones, Automotive, Other Applications

Subsegments:

1) By Hardware: AI Chips, Sensors, Mobile Devices

2) By Software: Machine Learning Algorithms, Natural Language Processing (NLP) Tools, AI Frameworks And Platforms, Mobile Applications With AI Capabilities

3) By Services: AI Consulting Services, AI Integration Services, AI Maintenance And Support Services, Custom AI Development Services

What Are the Current Trends Influencing the Mobile Artificial Intelligence Market?

Major companies operating in the mobile artificial intelligence market are adopting new technologies, such as generative AI to sustain their position in the market. Generative AI is a type of artificial intelligence technology that can produce various types of content, including text, imagery, audio, and synthetic data. For instance, in April 2023, Sofy, a US-based company that provides automation solutions for mobile apps, launched SofySense, a generative AI-driven, no-code mobile app testing solution. Generative AI can help create new data from existing data, while no-code testing solutions enable users to conduct software testing without writing code. This combination could revolutionize mobile app testing by automating the process and making it more efficient. SofySense reduces time spent reviewing outcomes to identify concerns by producing test cases, hindering research and test design requirements and enabling test cases to smoothly convert to automated tests rather than spending time creating automation code.

Who Are the Major Companies Operating in the Mobile Artificial Intelligence Market?

Major companies operating in the mobile artificial intelligence market are Apple Inc., Google LLC, Samsung Electronics Co Ltd., Microsoft Corporation, Alibaba Group Holding Limited, Tencent Holdings Limited, Amazon Web Services Inc., Intel Corporation, IBM Corporation, LG Electronics Inc., Qualcomm Incorporated, NVIDIA Corporation, Salesforce Inc., Nokia Corporation, MediaTek Inc., Baidu Inc., Cerebras Systems Inc., H2O.ai (http://H2O.ai) Inc., Fuzhou Rockchip Electronics Co Ltd., Cambricon Technologies Corporation Ltd., Huawei Technologies Co Ltd., Shanghai Thinkforce Electronic Technology Co Ltd, Blaize Inc., Kneron Inc., Graphcore Ltd., Deephi Technology Co Ltd.

Get the detailed mobile artificial intelligence market report today

Mobile Artificial Intelligence Market Forecast And Analysis (https://www.thebusinessresearchcompany.com/report/mobile-artificial-intelligence-global-market-report)

Which Region Holds the Largest Share of the Mobile Artificial Intelligence Market?

North America was the largest region in the mobile artificial intelligence market in 2024. Asia-Pacific is expected to be the fastest-growing region in the forecast period. The regions covered in mobile artificial intelligence market report are Asia-Pacific, Western Europe, Eastern Europe, North America, South America, Middle East and Africa.

#Contact Us:#

The Business Research Company: Market Research Reports (https://thebusinessresearchcompany.com/)

Americas +1 310-496-7795

Asia +44 7882 955267 & +91 8897263534

Europe +44 7882 955267

Email: info@tbrc.info (mailto:info@tbrc.info)

#Follow Us On:#

LinkedIn: The Business Research Company | LinkedIn (https://in.linkedin.com/company/the-business-research-company)

Use Code ONLINE20 to Save 20% On Global Market Reports – Gain Access to Trusted Market Data, Growth Indicators, and Industry Analytics

What Is the Current Size and Annual Growth Rate of the Mobile Artificial Intelligence Market?

The mobile artificial intelligence market size has grown exponentially in recent years. It will grow from $17.45 billion in 2024 to $22.15 billion in 2025 at a compound annual growth rate (CAGR) of 26.9%. The growth in the historic period can be attributed to growing adoption of smartphones and tablets, increasing research and development activities, increasing awareness of the ai-based solutions, growing dependency on iot devices.

The mobile artificial intelligence market size is expected to see exponential growth in the next few years. It will grow to $53.7 billion in 2029 at a compound annual growth rate (CAGR) of 24.8%. The growth in the forecast period can be attributed to increasing adoption of ai-based solutions across various industries, increasing power of mobile processors, development of new mobile ai software frameworks, growing demand for mobile ai applications. Major trends in the forecast period include ai chipsets, advancements in hardware, ai-powered mobile apps, edge ai, 5g connectivity.

Get your free report sample today:

Mobile Artificial Intelligence Market Forecast And Analysis Sample (https://www.thebusinessresearchcompany.com/sample.aspx?id=12875&type=smp)

What Are the Primary Factors Driving the Mobile Artificial Intelligence Market?

The increasing penetration of smartphones is expected to propel the growth of the mobile artificial intelligence market going forward. Smartphones are handheld electronic devices that combine the functionalities of a mobile phone and a personal computer. Smartphones play a significant role in implementing and using mobile artificial intelligence (AI) and serve as powerful and versatile platforms for mobile AI, enabling AI-driven functionalities, personalized experiences, intelligent interactions and on-the-go AI processing. For instance, in February 2023, according to Uswitch Limited, a UK-based price comparison and switching service company, there were 71.8 million mobile connections in the UK, a 3.8% (or around 2.6 million) increase over 2021. The UK population is expected to grow to 68.3 million by 2025, of which 95% (or about 65 million individuals) will own a smartphone. Therefore, the increasing penetration of smartphones will drive the growth of the mobile artificial intelligence market.

How Is the Mobile Artificial Intelligence Market Categorized Based on Key Segments?

The mobile artificial intelligencemarket covered in this report is segmented –

1) By Component: Hardware, Software, Services

2) By Technology Node: 20–28 Nano Meter (NM), 10 Nano Meter (NM), 7 Nano Meter (NM), Other Technology Nodes

3) By Application: Smartphones, Robotics, Augmented Reality (AR) And Virtual Reality(VR), Cameras, Drones, Automotive, Other Applications

Subsegments:

1) By Hardware: AI Chips, Sensors, Mobile Devices

2) By Software: Machine Learning Algorithms, Natural Language Processing (NLP) Tools, AI Frameworks And Platforms, Mobile Applications With AI Capabilities

3) By Services: AI Consulting Services, AI Integration Services, AI Maintenance And Support Services, Custom AI Development Services

What Are the Current Trends Influencing the Mobile Artificial Intelligence Market?

Major companies operating in the mobile artificial intelligence market are adopting new technologies, such as generative AI to sustain their position in the market. Generative AI is a type of artificial intelligence technology that can produce various types of content, including text, imagery, audio, and synthetic data. For instance, in April 2023, Sofy, a US-based company that provides automation solutions for mobile apps, launched SofySense, a generative AI-driven, no-code mobile app testing solution. Generative AI can help create new data from existing data, while no-code testing solutions enable users to conduct software testing without writing code. This combination could revolutionize mobile app testing by automating the process and making it more efficient. SofySense reduces time spent reviewing outcomes to identify concerns by producing test cases, hindering research and test design requirements and enabling test cases to smoothly convert to automated tests rather than spending time creating automation code.

Who Are the Major Companies Operating in the Mobile Artificial Intelligence Market?

Major companies operating in the mobile artificial intelligence market are Apple Inc., Google LLC, Samsung Electronics Co Ltd., Microsoft Corporation, Alibaba Group Holding Limited, Tencent Holdings Limited, Amazon Web Services Inc., Intel Corporation, IBM Corporation, LG Electronics Inc., Qualcomm Incorporated, NVIDIA Corporation, Salesforce Inc., Nokia Corporation, MediaTek Inc., Baidu Inc., Cerebras Systems Inc., H2O.ai (http://H2O.ai) Inc., Fuzhou Rockchip Electronics Co Ltd., Cambricon Technologies Corporation Ltd., Huawei Technologies Co Ltd., Shanghai Thinkforce Electronic Technology Co Ltd, Blaize Inc., Kneron Inc., Graphcore Ltd., Deephi Technology Co Ltd.

Get the detailed mobile artificial intelligence market report today

Mobile Artificial Intelligence Market Forecast And Analysis (https://www.thebusinessresearchcompany.com/report/mobile-artificial-intelligence-global-market-report)

Which Region Holds the Largest Share of the Mobile Artificial Intelligence Market?

North America was the largest region in the mobile artificial intelligence market in 2024. Asia-Pacific is expected to be the fastest-growing region in the forecast period. The regions covered in mobile artificial intelligence market report are Asia-Pacific, Western Europe, Eastern Europe, North America, South America, Middle East and Africa.

#Contact Us:#

The Business Research Company: Market Research Reports (https://thebusinessresearchcompany.com/)

Americas +1 310-496-7795

Asia +44 7882 955267 & +91 8897263534

Europe +44 7882 955267

Email: info@tbrc.info (mailto:info@tbrc.info)

#Follow Us On:#

LinkedIn: The Business Research Company | LinkedIn (https://in.linkedin.com/company/the-business-research-company)

Global Mobile Artificial Intelligence Market Anticipated to Expand Rapidly From 2025 to 2029

Use Code ONLINE20 to Save 20% On Global Market Reports – Gain Access to Trusted Market Data, Growth Indicators, and Industry Analytics

What Is the Current Size and Annual Growth Rate of the Mobile Artificial Intelligence Market?

The mobile artificial intelligence market size has grown exponentially in recent years. It will grow from $17.45 billion in 2024 to $22.15 billion in 2025 at a compound annual growth rate (CAGR) of 26.9%. The growth in the historic period can be attributed to growing adoption of smartphones and tablets, increasing research and development activities, increasing awareness of the ai-based solutions, growing dependency on iot devices.

The mobile artificial intelligence market size is expected to see exponential growth in the next few years. It will grow to $53.7 billion in 2029 at a compound annual growth rate (CAGR) of 24.8%. The growth in the forecast period can be attributed to increasing adoption of ai-based solutions across various industries, increasing power of mobile processors, development of new mobile ai software frameworks, growing demand for mobile ai applications. Major trends in the forecast period include ai chipsets, advancements in hardware, ai-powered mobile apps, edge ai, 5g connectivity.

Get your free report sample today:

Mobile Artificial Intelligence Market Forecast And Analysis Sample (https://www.thebusinessresearchcompany.com/sample.aspx?id=12875&type=smp)

What Are the Primary Factors Driving the Mobile Artificial Intelligence Market?

The increasing penetration of smartphones is expected to propel the growth of the mobile artificial intelligence market going forward. Smartphones are handheld electronic devices that combine the functionalities of a mobile phone and a personal computer. Smartphones play a significant role in implementing and using mobile artificial intelligence (AI) and serve as powerful and versatile platforms for mobile AI, enabling AI-driven functionalities, personalized experiences, intelligent interactions and on-the-go AI processing. For instance, in February 2023, according to Uswitch Limited, a UK-based price comparison and switching service company, there were 71.8 million mobile connections in the UK, a 3.8% (or around 2.6 million) increase over 2021. The UK population is expected to grow to 68.3 million by 2025, of which 95% (or about 65 million individuals) will own a smartphone. Therefore, the increasing penetration of smartphones will drive the growth of the mobile artificial intelligence market.

How Is the Mobile Artificial Intelligence Market Categorized Based on Key Segments?

The mobile artificial intelligencemarket covered in this report is segmented –

1) By Component: Hardware, Software, Services

2) By Technology Node: 20–28 Nano Meter (NM), 10 Nano Meter (NM), 7 Nano Meter (NM), Other Technology Nodes

3) By Application: Smartphones, Robotics, Augmented Reality (AR) And Virtual Reality(VR), Cameras, Drones, Automotive, Other Applications

Subsegments:

1) By Hardware: AI Chips, Sensors, Mobile Devices

2) By Software: Machine Learning Algorithms, Natural Language Processing (NLP) Tools, AI Frameworks And Platforms, Mobile Applications With AI Capabilities

3) By Services: AI Consulting Services, AI Integration Services, AI Maintenance And Support Services, Custom AI Development Services

What Are the Current Trends Influencing the Mobile Artificial Intelligence Market?

Major companies operating in the mobile artificial intelligence market are adopting new technologies, such as generative AI to sustain their position in the market. Generative AI is a type of artificial intelligence technology that can produce various types of content, including text, imagery, audio, and synthetic data. For instance, in April 2023, Sofy, a US-based company that provides automation solutions for mobile apps, launched SofySense, a generative AI-driven, no-code mobile app testing solution. Generative AI can help create new data from existing data, while no-code testing solutions enable users to conduct software testing without writing code. This combination could revolutionize mobile app testing by automating the process and making it more efficient. SofySense reduces time spent reviewing outcomes to identify concerns by producing test cases, hindering research and test design requirements and enabling test cases to smoothly convert to automated tests rather than spending time creating automation code.

Who Are the Major Companies Operating in the Mobile Artificial Intelligence Market?

Major companies operating in the mobile artificial intelligence market are Apple Inc., Google LLC, Samsung Electronics Co Ltd., Microsoft Corporation, Alibaba Group Holding Limited, Tencent Holdings Limited, Amazon Web Services Inc., Intel Corporation, IBM Corporation, LG Electronics Inc., Qualcomm Incorporated, NVIDIA Corporation, Salesforce Inc., Nokia Corporation, MediaTek Inc., Baidu Inc., Cerebras Systems Inc., H2O.ai (http://H2O.ai) Inc., Fuzhou Rockchip Electronics Co Ltd., Cambricon Technologies Corporation Ltd., Huawei Technologies Co Ltd., Shanghai Thinkforce Electronic Technology Co Ltd, Blaize Inc., Kneron Inc., Graphcore Ltd., Deephi Technology Co Ltd.

Get the detailed mobile artificial intelligence market report today

Mobile Artificial Intelligence Market Forecast And Analysis (https://www.thebusinessresearchcompany.com/report/mobile-artificial-intelligence-global-market-report)

Which Region Holds the Largest Share of the Mobile Artificial Intelligence Market?

North America was the largest region in the mobile artificial intelligence market in 2024. Asia-Pacific is expected to be the fastest-growing region in the forecast period. The regions covered in mobile artificial intelligence market report are Asia-Pacific, Western Europe, Eastern Europe, North America, South America, Middle East and Africa.

#Contact Us:#

The Business Research Company: Market Research Reports (https://thebusinessresearchcompany.com/)

Americas +1 310-496-7795

Asia +44 7882 955267 & +91 8897263534

Europe +44 7882 955267

Email: info@tbrc.info (mailto:info@tbrc.info)

#Follow Us On:#

LinkedIn: The Business Research Company | LinkedIn (https://in.linkedin.com/company/the-business-research-company)

0 Commenti

0 Condivisioni

6K Visualizzazioni