Global Mass Transit Security Market Projected to Strengthen in Value and Scale by 2029

Grab 20% Off With Code ONLINE20 On Global market Reports – Evaluate Global Trends, Market Risks, and Competitive Intelligence

What Is the Predicted Market Size and CAGR of the Mass Transit Security Market by the End of the 2029?

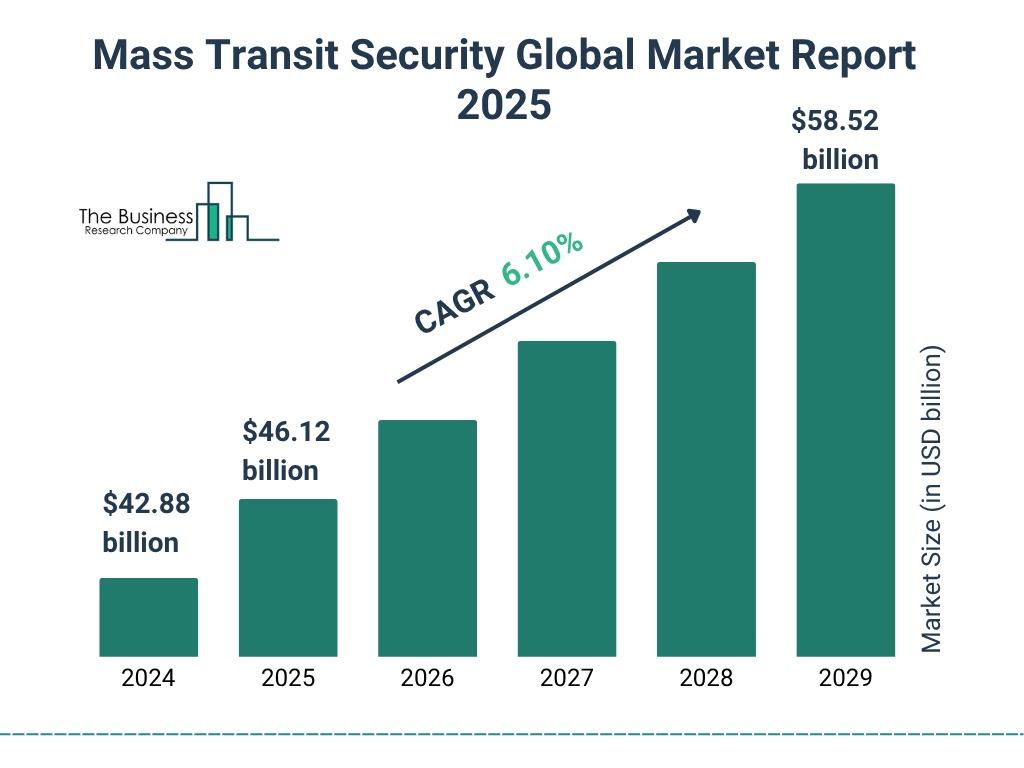

The mass transit security market size has grown strongly in recent years. It will grow from $42.88 billion in 2024 to $46.12 billion in 2025 at a compound annual growth rate (CAGR) of 7.6%. The growth in the historic period can be attributed to public transportation systems, demand for innovative security solutions, increased investments in advanced surveillance, increased access control systems, increased biometrics, security breaches.

The mass transit security market size is expected to see strong growth in the next few years. It will grow to $58.52 billion in 2029 at a compound annual growth rate (CAGR) of 6.1%. The growth in the forecast period can be attributed to increasing public incidents, deployment of biometric identification systems, terrorism threats, public awareness and cooperation, geopolitical tensions. Major trends in the forecast period include AI-driven threat detection, enhanced biometric identification, internet of things (IoT) security, mobile security solutions, drone detection and mitigation.

Get your free report sample today:

Mass Transit Security Market Report 2025, Growth and Analysis Sample (https://www.thebusinessresearchcompany.com/sample.aspx?id=14133&type=smp)

What Are the Significant Market Forces Driving the Mass Transit Security Market Performance?

The increasing threats and security concerns are expected to propel the growth of the mass transit security market going forward. Security threats and concerns refer to any potential danger or harmful event that can exploit a vulnerability and cause harm to any personnel. Public transit environments may be susceptible to criminal activities, including theft, assaults, and vandalism. Mass transit security plays a crucial role in addressing threats and security concerns by implementing measures to protect passengers, infrastructure, and operations from various risks. For instance, in April 2024, according to the Department for Science, Innovation and Technology, a UK-based government department, An estimated 22% of businesses and 14% of charities have encountered cyber crime in the past year. This figure increases to 45% for medium-sized businesses, 58% for large businesses, and 37% for high-income charities. Alternatively, among the 50% of businesses and 32% of charities reporting any cybersecurity breaches or attacks, just over two-fifths (44% of businesses and 42% of charities) ultimately fell victim to cyber crime. Therefore, increasing threats and security concerns are driving the mass transit security market.

Which Segments Are Likely to Shape the Future Outlook of the Mass Transit Security Market?

The mass transit securitymarket covered in this report is segmented –

1) By Type: Airways Transit Security, Seaways Transit Security, Roadways Transit Security, Railways Transit Security, Other Types

2) By Service Type: Managed Services, Professional Services

3) By Solution: Surveillance and Monitoring, Screening System, Biometric Security And Authentication System, Fire Safety And Detection System, Perimeter Intrusion Detection, Access Control, Other Solutions

4) By Application: Homeland Security, Industrial, Retail And Payment Industries, Logistics And Transportation Industries, Healthcare, Other Applications

Subsegments:

1) By Airways Transit Security: Airport Security Screening, Passenger And Baggage Screening, Perimeter Security Systems

2) By Seaways Transit Security: Port Security Solutions, Vessel Monitoring Systems, Cargo Security Measures

3) By Roadways Transit Security: Vehicle Surveillance Systems, Traffic Management Solutions, Emergency Response Systems

4) By Railways Transit Security: Train Surveillance Systems, Station Security Solutions, Rail Network Monitoring

5) By Other Types: Emergency Services Security, Public Transport Security Systems, Event Security Management

What New Market Trends Are Emerging in the Mass Transit Security Market?

Major companies operating in the mass transit security market are focusing on developing new technologies, such as AI-enabled video analytics platform. This platform process actionable insights and conclusions from digital video using AI techniques. For instance, in October 2024, PRAMA, an India-based manufacturer of video security products, launched transport security innovations, including AI-based cameras and traffic management solutions. PRAMA's transportation solutions uniquely focus on securing transportation hubs with advanced video surveillance systems, featuring a Command and Control solution for proactive video data monitoring. These products are specifically designed to enhance vehicle security and traffic management, ensuring a safe and efficient flow for travelers, vehicles, and pedestrians alike.

Which Major Organizations Influence the Direction of the Mass Transit Security Market?

Major companies operating in the mass transit security market are Siemens AG, Panasonic Corporation, Cisco Systems Inc., Hanwha Group, Honeywell International Inc, Johnson Controls International PLC, Thales Group, Tyco International PLC, L3Harris Technologies Inc, Analog Devices Inc., Hikvision Digital Technology Co. Ltd, Bosch Security Systems Inc., NICE Systems Ltd., Axis Communications AB, OSI Systems Inc, Kratos Defense & Security Solutions Inc. (KTOS), Flir Systems Inc., Smiths Detection Inc, Avigilon Corporation, Nuctech Company Limited, Rapiscan Systems Inc, Genetec Inc., Analogic Corporation, Teleste, SDI Presence LLC, March Networks Corporation, IndigoVision Group PLC, High Rise Security Systems LLC, AngelTrax, Fortem Technologies Inc.

Get the detailed mass transit security market report today

Mass Transit Security Market Report 2025, Growth and Analysis (https://www.thebusinessresearchcompany.com/report/mass-transit-security-global-market-report)

Which Region Holds the Largest Share of the Mass Transit Security Market?

North America was the largest region in the mass transit security market in 2024. Asia-Pacific is expected to be the fastest-growing region in the forecast period. The regions covered in the mass transit security market report are Asia-Pacific, Western Europe, Eastern Europe, North America, South America, Middle East, Africa.

#Contact Us:#

The Business Research Company: Market Research Reports (https://thebusinessresearchcompany.com/)

Americas +1 310-496-7795

Asia +44 7882 955267 & +91 8897263534

Europe +44 7882 955267

Email: info@tbrc.info (mailto:info@tbrc.info)

#Follow Us On:#

LinkedIn: The Business Research Company | LinkedIn (https://in.linkedin.com/company/the-business-research-company)

Grab 20% Off With Code ONLINE20 On Global market Reports – Evaluate Global Trends, Market Risks, and Competitive Intelligence

What Is the Predicted Market Size and CAGR of the Mass Transit Security Market by the End of the 2029?

The mass transit security market size has grown strongly in recent years. It will grow from $42.88 billion in 2024 to $46.12 billion in 2025 at a compound annual growth rate (CAGR) of 7.6%. The growth in the historic period can be attributed to public transportation systems, demand for innovative security solutions, increased investments in advanced surveillance, increased access control systems, increased biometrics, security breaches.

The mass transit security market size is expected to see strong growth in the next few years. It will grow to $58.52 billion in 2029 at a compound annual growth rate (CAGR) of 6.1%. The growth in the forecast period can be attributed to increasing public incidents, deployment of biometric identification systems, terrorism threats, public awareness and cooperation, geopolitical tensions. Major trends in the forecast period include AI-driven threat detection, enhanced biometric identification, internet of things (IoT) security, mobile security solutions, drone detection and mitigation.

Get your free report sample today:

Mass Transit Security Market Report 2025, Growth and Analysis Sample (https://www.thebusinessresearchcompany.com/sample.aspx?id=14133&type=smp)

What Are the Significant Market Forces Driving the Mass Transit Security Market Performance?

The increasing threats and security concerns are expected to propel the growth of the mass transit security market going forward. Security threats and concerns refer to any potential danger or harmful event that can exploit a vulnerability and cause harm to any personnel. Public transit environments may be susceptible to criminal activities, including theft, assaults, and vandalism. Mass transit security plays a crucial role in addressing threats and security concerns by implementing measures to protect passengers, infrastructure, and operations from various risks. For instance, in April 2024, according to the Department for Science, Innovation and Technology, a UK-based government department, An estimated 22% of businesses and 14% of charities have encountered cyber crime in the past year. This figure increases to 45% for medium-sized businesses, 58% for large businesses, and 37% for high-income charities. Alternatively, among the 50% of businesses and 32% of charities reporting any cybersecurity breaches or attacks, just over two-fifths (44% of businesses and 42% of charities) ultimately fell victim to cyber crime. Therefore, increasing threats and security concerns are driving the mass transit security market.

Which Segments Are Likely to Shape the Future Outlook of the Mass Transit Security Market?

The mass transit securitymarket covered in this report is segmented –

1) By Type: Airways Transit Security, Seaways Transit Security, Roadways Transit Security, Railways Transit Security, Other Types

2) By Service Type: Managed Services, Professional Services

3) By Solution: Surveillance and Monitoring, Screening System, Biometric Security And Authentication System, Fire Safety And Detection System, Perimeter Intrusion Detection, Access Control, Other Solutions

4) By Application: Homeland Security, Industrial, Retail And Payment Industries, Logistics And Transportation Industries, Healthcare, Other Applications

Subsegments:

1) By Airways Transit Security: Airport Security Screening, Passenger And Baggage Screening, Perimeter Security Systems

2) By Seaways Transit Security: Port Security Solutions, Vessel Monitoring Systems, Cargo Security Measures

3) By Roadways Transit Security: Vehicle Surveillance Systems, Traffic Management Solutions, Emergency Response Systems

4) By Railways Transit Security: Train Surveillance Systems, Station Security Solutions, Rail Network Monitoring

5) By Other Types: Emergency Services Security, Public Transport Security Systems, Event Security Management

What New Market Trends Are Emerging in the Mass Transit Security Market?

Major companies operating in the mass transit security market are focusing on developing new technologies, such as AI-enabled video analytics platform. This platform process actionable insights and conclusions from digital video using AI techniques. For instance, in October 2024, PRAMA, an India-based manufacturer of video security products, launched transport security innovations, including AI-based cameras and traffic management solutions. PRAMA's transportation solutions uniquely focus on securing transportation hubs with advanced video surveillance systems, featuring a Command and Control solution for proactive video data monitoring. These products are specifically designed to enhance vehicle security and traffic management, ensuring a safe and efficient flow for travelers, vehicles, and pedestrians alike.

Which Major Organizations Influence the Direction of the Mass Transit Security Market?

Major companies operating in the mass transit security market are Siemens AG, Panasonic Corporation, Cisco Systems Inc., Hanwha Group, Honeywell International Inc, Johnson Controls International PLC, Thales Group, Tyco International PLC, L3Harris Technologies Inc, Analog Devices Inc., Hikvision Digital Technology Co. Ltd, Bosch Security Systems Inc., NICE Systems Ltd., Axis Communications AB, OSI Systems Inc, Kratos Defense & Security Solutions Inc. (KTOS), Flir Systems Inc., Smiths Detection Inc, Avigilon Corporation, Nuctech Company Limited, Rapiscan Systems Inc, Genetec Inc., Analogic Corporation, Teleste, SDI Presence LLC, March Networks Corporation, IndigoVision Group PLC, High Rise Security Systems LLC, AngelTrax, Fortem Technologies Inc.

Get the detailed mass transit security market report today

Mass Transit Security Market Report 2025, Growth and Analysis (https://www.thebusinessresearchcompany.com/report/mass-transit-security-global-market-report)

Which Region Holds the Largest Share of the Mass Transit Security Market?

North America was the largest region in the mass transit security market in 2024. Asia-Pacific is expected to be the fastest-growing region in the forecast period. The regions covered in the mass transit security market report are Asia-Pacific, Western Europe, Eastern Europe, North America, South America, Middle East, Africa.

#Contact Us:#

The Business Research Company: Market Research Reports (https://thebusinessresearchcompany.com/)

Americas +1 310-496-7795

Asia +44 7882 955267 & +91 8897263534

Europe +44 7882 955267

Email: info@tbrc.info (mailto:info@tbrc.info)

#Follow Us On:#

LinkedIn: The Business Research Company | LinkedIn (https://in.linkedin.com/company/the-business-research-company)

Global Mass Transit Security Market Projected to Strengthen in Value and Scale by 2029

Grab 20% Off With Code ONLINE20 On Global market Reports – Evaluate Global Trends, Market Risks, and Competitive Intelligence

What Is the Predicted Market Size and CAGR of the Mass Transit Security Market by the End of the 2029?

The mass transit security market size has grown strongly in recent years. It will grow from $42.88 billion in 2024 to $46.12 billion in 2025 at a compound annual growth rate (CAGR) of 7.6%. The growth in the historic period can be attributed to public transportation systems, demand for innovative security solutions, increased investments in advanced surveillance, increased access control systems, increased biometrics, security breaches.

The mass transit security market size is expected to see strong growth in the next few years. It will grow to $58.52 billion in 2029 at a compound annual growth rate (CAGR) of 6.1%. The growth in the forecast period can be attributed to increasing public incidents, deployment of biometric identification systems, terrorism threats, public awareness and cooperation, geopolitical tensions. Major trends in the forecast period include AI-driven threat detection, enhanced biometric identification, internet of things (IoT) security, mobile security solutions, drone detection and mitigation.

Get your free report sample today:

Mass Transit Security Market Report 2025, Growth and Analysis Sample (https://www.thebusinessresearchcompany.com/sample.aspx?id=14133&type=smp)

What Are the Significant Market Forces Driving the Mass Transit Security Market Performance?

The increasing threats and security concerns are expected to propel the growth of the mass transit security market going forward. Security threats and concerns refer to any potential danger or harmful event that can exploit a vulnerability and cause harm to any personnel. Public transit environments may be susceptible to criminal activities, including theft, assaults, and vandalism. Mass transit security plays a crucial role in addressing threats and security concerns by implementing measures to protect passengers, infrastructure, and operations from various risks. For instance, in April 2024, according to the Department for Science, Innovation and Technology, a UK-based government department, An estimated 22% of businesses and 14% of charities have encountered cyber crime in the past year. This figure increases to 45% for medium-sized businesses, 58% for large businesses, and 37% for high-income charities. Alternatively, among the 50% of businesses and 32% of charities reporting any cybersecurity breaches or attacks, just over two-fifths (44% of businesses and 42% of charities) ultimately fell victim to cyber crime. Therefore, increasing threats and security concerns are driving the mass transit security market.

Which Segments Are Likely to Shape the Future Outlook of the Mass Transit Security Market?

The mass transit securitymarket covered in this report is segmented –

1) By Type: Airways Transit Security, Seaways Transit Security, Roadways Transit Security, Railways Transit Security, Other Types

2) By Service Type: Managed Services, Professional Services

3) By Solution: Surveillance and Monitoring, Screening System, Biometric Security And Authentication System, Fire Safety And Detection System, Perimeter Intrusion Detection, Access Control, Other Solutions

4) By Application: Homeland Security, Industrial, Retail And Payment Industries, Logistics And Transportation Industries, Healthcare, Other Applications

Subsegments:

1) By Airways Transit Security: Airport Security Screening, Passenger And Baggage Screening, Perimeter Security Systems

2) By Seaways Transit Security: Port Security Solutions, Vessel Monitoring Systems, Cargo Security Measures

3) By Roadways Transit Security: Vehicle Surveillance Systems, Traffic Management Solutions, Emergency Response Systems

4) By Railways Transit Security: Train Surveillance Systems, Station Security Solutions, Rail Network Monitoring

5) By Other Types: Emergency Services Security, Public Transport Security Systems, Event Security Management

What New Market Trends Are Emerging in the Mass Transit Security Market?

Major companies operating in the mass transit security market are focusing on developing new technologies, such as AI-enabled video analytics platform. This platform process actionable insights and conclusions from digital video using AI techniques. For instance, in October 2024, PRAMA, an India-based manufacturer of video security products, launched transport security innovations, including AI-based cameras and traffic management solutions. PRAMA's transportation solutions uniquely focus on securing transportation hubs with advanced video surveillance systems, featuring a Command and Control solution for proactive video data monitoring. These products are specifically designed to enhance vehicle security and traffic management, ensuring a safe and efficient flow for travelers, vehicles, and pedestrians alike.

Which Major Organizations Influence the Direction of the Mass Transit Security Market?

Major companies operating in the mass transit security market are Siemens AG, Panasonic Corporation, Cisco Systems Inc., Hanwha Group, Honeywell International Inc, Johnson Controls International PLC, Thales Group, Tyco International PLC, L3Harris Technologies Inc, Analog Devices Inc., Hikvision Digital Technology Co. Ltd, Bosch Security Systems Inc., NICE Systems Ltd., Axis Communications AB, OSI Systems Inc, Kratos Defense & Security Solutions Inc. (KTOS), Flir Systems Inc., Smiths Detection Inc, Avigilon Corporation, Nuctech Company Limited, Rapiscan Systems Inc, Genetec Inc., Analogic Corporation, Teleste, SDI Presence LLC, March Networks Corporation, IndigoVision Group PLC, High Rise Security Systems LLC, AngelTrax, Fortem Technologies Inc.

Get the detailed mass transit security market report today

Mass Transit Security Market Report 2025, Growth and Analysis (https://www.thebusinessresearchcompany.com/report/mass-transit-security-global-market-report)

Which Region Holds the Largest Share of the Mass Transit Security Market?

North America was the largest region in the mass transit security market in 2024. Asia-Pacific is expected to be the fastest-growing region in the forecast period. The regions covered in the mass transit security market report are Asia-Pacific, Western Europe, Eastern Europe, North America, South America, Middle East, Africa.

#Contact Us:#

The Business Research Company: Market Research Reports (https://thebusinessresearchcompany.com/)

Americas +1 310-496-7795

Asia +44 7882 955267 & +91 8897263534

Europe +44 7882 955267

Email: info@tbrc.info (mailto:info@tbrc.info)

#Follow Us On:#

LinkedIn: The Business Research Company | LinkedIn (https://in.linkedin.com/company/the-business-research-company)

0 Comentários

0 Compartilhamentos

3K Visualizações