Global Solar Photovoltaic (PV) Panels Market to Reach USD 76,160 Million by 2032, Growing at 9.2% CAGR

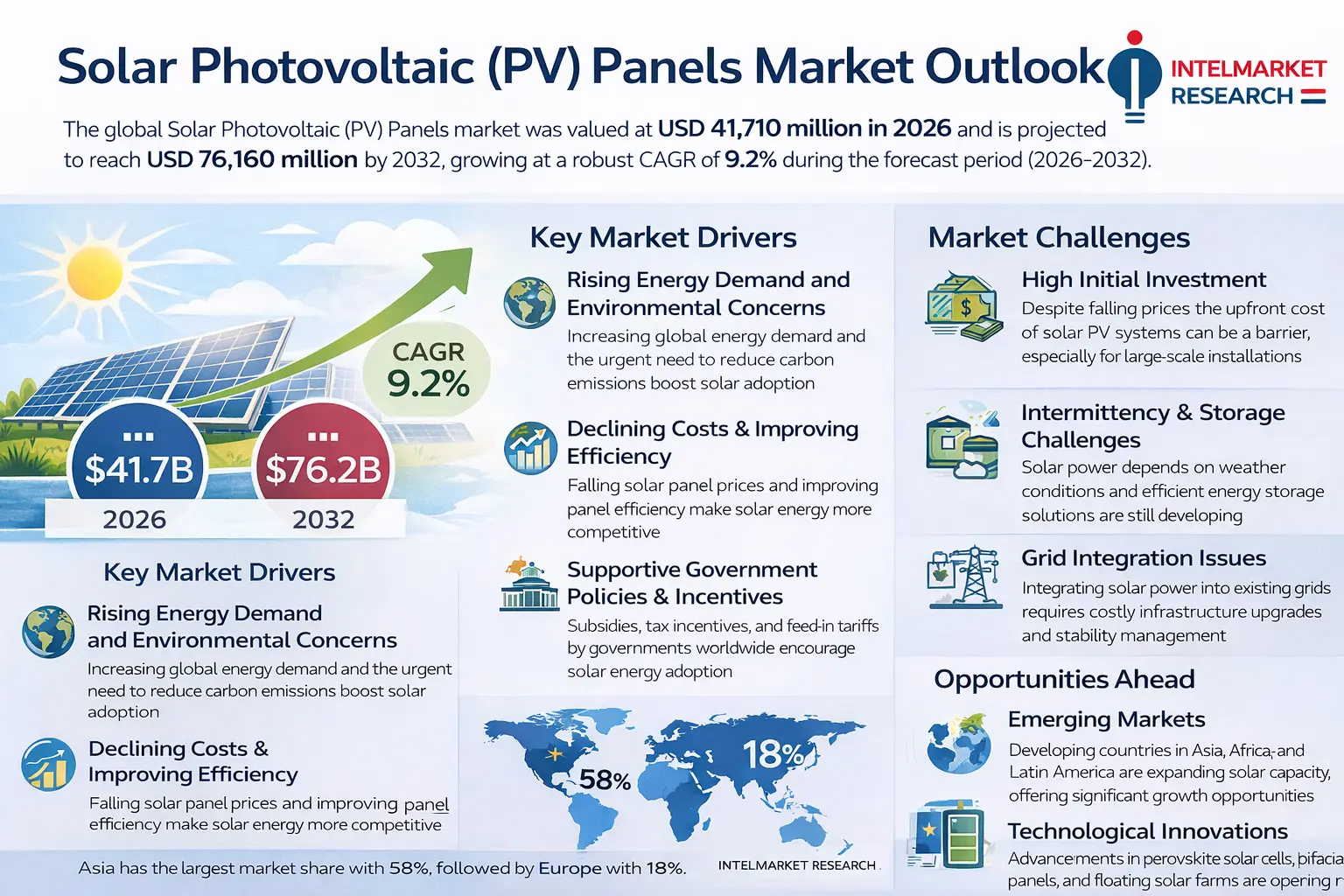

According to a new report from Intel Market Research, Global Solar Photovoltaic (PV) Panels market was valued at USD 41,710 million in 2025 and is projected to reach USD 76,160 million by 2032, growing at a robust CAGR of 9.2% during the forecast period (2026-2032). This growth is propelled by the increasing global demand for clean energy, supportive government policies, declining solar panel prices, and growing environmental consciousness worldwide.

What are Solar Photovoltaic (PV) Panels?

A solar cell or photovoltaic (PV) cell is a semiconductor device that converts light directly into electricity by the photovoltaic effect. The most common material in solar cell production is purified silicon that can be applied in different ways. A (Solar Photovoltaic (PV) Panels) PV module is an assembly of photo-voltaic cells mounted in a framework for installation. Photo-voltaic cells use sunlight as a source of energy and generate direct current electricity. A collection of PV modules is called a PV Panel, and a system of Panels is an Array. Arrays of a photovoltaic system supply solar electricity to electrical equipment.

Asia is the largest Solar Photovoltaic (PV) Panels market with about 58% market share. Europe is the follower with about 18% market share.

Download Sample Report:

https://www.intelmarketresearch.com/solar-photovoltaic-panels-market-11351

Key Market Drivers

1. Rising Energy Demand and Environmental Concerns

The increasing global energy demand, coupled with growing environmental concerns and the need to reduce carbon emissions, is driving the adoption of solar photovoltaic technology. Governments worldwide are setting ambitious renewable energy targets, with many aiming for carbon neutrality by 2050, creating substantial demand for solar panels.

2. Declining Costs and Improving Efficiency

Solar panel prices have dropped significantly over the past decade due to technological advancements, economies of scale, and increased manufacturing competition. Meanwhile, the efficiency of solar panels has been steadily improving, making solar energy more competitive with traditional energy sources.

3. Supportive Government Policies and Incentives

Many governments offer subsidies, tax incentives, feed-in tariffs, and other financial incentives to promote solar energy adoption. These policies make solar investments more attractive to both utility companies and individual consumers.

Market Challenges

1. High Initial Investment

Despite declining prices, the initial investment for solar PV systems remains substantial, especially for large-scale installations. This can be a barrier for widespread adoption, particularly in developing regions.

2. Intermittency and Storage Challenges

Solar energy generation is intermittent and depends on weather conditions. The lack of efficient and cost-effective energy storage solutions remains a challenge for providing consistent power supply.

3. Grid Integration Issues

Integrating large amounts of solar power into existing electrical grids requires infrastructure upgrades and can create stability challenges if not managed properly.

Opportunities Ahead

1. Emerging Markets

Many developing countries in Asia, Africa, and Latin America are rapidly expanding their solar capacity. These markets offer significant growth opportunities as they seek to meet growing energy demands with clean sources.

2. Technological Innovations

Ongoing research in perovskite solar cells, bifacial panels, floating solar farms, and building-integrated photovoltaics (BIPV) is opening new application areas and improving efficiency.

3. Energy Storage Integration

Advancements in battery technology, particularly lithium-ion and emerging technologies, are making solar-plus-storage systems more viable, helping to overcome intermittency challenges.

Regional Market Insights

1. Asia-Pacific Dominance

Asia-Pacific is the largest and fastest-growing market for solar PV panels, with China leading in both production and installation. India, Japan, and South Korea are also significant markets with ambitious solar expansion plans.

2. European Market

Europe has been a traditional leader in solar adoption, with Germany, Spain, Italy, and more recently, Netherlands and Poland showing strong growth. The European Green Deal is expected to further accelerate solar adoption.

3. North American Market

The United States and Canada have seen consistent growth in solar installations, supported by federal and state-level policies. The U.S. is one of the top markets globally.

4. Emerging Markets

Countries in Latin America, Middle East, and Africa are increasingly investing in solar energy, though from a smaller base. These regions offer substantial growth potential as costs continue to decline.

Market Segmentation

By Type

Mono-Si Modules

Multi-Si Modules

CdTe Modules

CIGS Modules

A-Si Modules

Others

By Application

PV Power Station

Commercial

Residential

Others

By End User

Utilities

Commercial & Industrial

Residential

Government

Download Sample Report:

https://www.intelmarketresearch.com/download-free-sample/11351/solar-photovoltaic-panels-2025-2032-229

Competitive Landscape

The global Solar Photovoltaic (PV) Panels market is highly competitive with several key players. The top 3 brands account for almost 40% revenue market share. Key players include:

LONGi

JinkoSolar

JA Solar

Trina Solar

Canadian Solar

Hanwha Solutions

Risen Energy

First Solar

Chint Electrics

GCL System

SunPower

Solargiga

Shunfeng

EGing PV

Seraphim

Jinergy

LG Business Solutions

Jolywood

Tangshan Haitai

HT-SAAE

Talesun Solar

These companies compete on factors such as price, efficiency, durability, warranty, and after-sales service. The market has seen increasing consolidation as companies seek economies of scale and geographic expansion.

Download Sample Report: Solar Photovoltaic (PV) Panels Market - View in Detailed Research Report

Future Outlook

The solar PV market is expected to continue its strong growth trajectory through the forecast period and beyond. Key trends to watch include:

Further Cost Reductions: Continued technological improvements and manufacturing scale will drive costs down further, making solar even more competitive.

Green Hydrogen Integration: Solar PV can power green hydrogen production, creating new synergies in the renewable energy ecosystem.

Floating Solar: Installing solar panels on water bodies is gaining popularity, especially in countries with land constraints.

Agrivoltaics: Combining solar energy generation with agriculture offers mutual benefits and land-use efficiency.

As the world continues to transition toward renewable energy, solar PV is expected to maintain its position as one of the fastest-growing energy sources. By 2032, solar is projected to become the largest source of electricity generation in many regions.

Download Sample Report: Solar Photovoltaic (PV) Panels Market - View in Detailed Research Report

About Intel Market Research

Intel Market Research is a leading provider of strategic intelligence, offering actionable insights in energy, technology, and industrial sectors. Our research capabilities include:

Real-time market monitoring and analysis

Supply chain and manufacturing intelligence

Policy and regulatory impact analysis

Competitive benchmarking and strategy

Trusted by Fortune 500 companies, our insights empower decision-makers to drive innovation with confidence.

Website:

https://www.intelmarketresearch.com

International: +1 (332) 2424 294

Asia-Pacific: +91 9169164321

LinkedIn: Follow Us

Global Solar Photovoltaic (PV) Panels Market to Reach USD 76,160 Million by 2032, Growing at 9.2% CAGR

According to a new report from Intel Market Research, Global Solar Photovoltaic (PV) Panels market was valued at USD 41,710 million in 2025 and is projected to reach USD 76,160 million by 2032, growing at a robust CAGR of 9.2% during the forecast period (2026-2032). This growth is propelled by the increasing global demand for clean energy, supportive government policies, declining solar panel prices, and growing environmental consciousness worldwide.

What are Solar Photovoltaic (PV) Panels?

A solar cell or photovoltaic (PV) cell is a semiconductor device that converts light directly into electricity by the photovoltaic effect. The most common material in solar cell production is purified silicon that can be applied in different ways. A (Solar Photovoltaic (PV) Panels) PV module is an assembly of photo-voltaic cells mounted in a framework for installation. Photo-voltaic cells use sunlight as a source of energy and generate direct current electricity. A collection of PV modules is called a PV Panel, and a system of Panels is an Array. Arrays of a photovoltaic system supply solar electricity to electrical equipment.

Asia is the largest Solar Photovoltaic (PV) Panels market with about 58% market share. Europe is the follower with about 18% market share.

📥 Download Sample Report: https://www.intelmarketresearch.com/solar-photovoltaic-panels-market-11351

Key Market Drivers

1. Rising Energy Demand and Environmental Concerns

The increasing global energy demand, coupled with growing environmental concerns and the need to reduce carbon emissions, is driving the adoption of solar photovoltaic technology. Governments worldwide are setting ambitious renewable energy targets, with many aiming for carbon neutrality by 2050, creating substantial demand for solar panels.

2. Declining Costs and Improving Efficiency

Solar panel prices have dropped significantly over the past decade due to technological advancements, economies of scale, and increased manufacturing competition. Meanwhile, the efficiency of solar panels has been steadily improving, making solar energy more competitive with traditional energy sources.

3. Supportive Government Policies and Incentives

Many governments offer subsidies, tax incentives, feed-in tariffs, and other financial incentives to promote solar energy adoption. These policies make solar investments more attractive to both utility companies and individual consumers.

Market Challenges

1. High Initial Investment

Despite declining prices, the initial investment for solar PV systems remains substantial, especially for large-scale installations. This can be a barrier for widespread adoption, particularly in developing regions.

2. Intermittency and Storage Challenges

Solar energy generation is intermittent and depends on weather conditions. The lack of efficient and cost-effective energy storage solutions remains a challenge for providing consistent power supply.

3. Grid Integration Issues

Integrating large amounts of solar power into existing electrical grids requires infrastructure upgrades and can create stability challenges if not managed properly.

Opportunities Ahead

1. Emerging Markets

Many developing countries in Asia, Africa, and Latin America are rapidly expanding their solar capacity. These markets offer significant growth opportunities as they seek to meet growing energy demands with clean sources.

2. Technological Innovations

Ongoing research in perovskite solar cells, bifacial panels, floating solar farms, and building-integrated photovoltaics (BIPV) is opening new application areas and improving efficiency.

3. Energy Storage Integration

Advancements in battery technology, particularly lithium-ion and emerging technologies, are making solar-plus-storage systems more viable, helping to overcome intermittency challenges.

Regional Market Insights

1. Asia-Pacific Dominance

Asia-Pacific is the largest and fastest-growing market for solar PV panels, with China leading in both production and installation. India, Japan, and South Korea are also significant markets with ambitious solar expansion plans.

2. European Market

Europe has been a traditional leader in solar adoption, with Germany, Spain, Italy, and more recently, Netherlands and Poland showing strong growth. The European Green Deal is expected to further accelerate solar adoption.

3. North American Market

The United States and Canada have seen consistent growth in solar installations, supported by federal and state-level policies. The U.S. is one of the top markets globally.

4. Emerging Markets

Countries in Latin America, Middle East, and Africa are increasingly investing in solar energy, though from a smaller base. These regions offer substantial growth potential as costs continue to decline.

Market Segmentation

By Type

Mono-Si Modules

Multi-Si Modules

CdTe Modules

CIGS Modules

A-Si Modules

Others

By Application

PV Power Station

Commercial

Residential

Others

By End User

Utilities

Commercial & Industrial

Residential

Government

📥 Download Sample Report: https://www.intelmarketresearch.com/download-free-sample/11351/solar-photovoltaic-panels-2025-2032-229

Competitive Landscape

The global Solar Photovoltaic (PV) Panels market is highly competitive with several key players. The top 3 brands account for almost 40% revenue market share. Key players include:

LONGi

JinkoSolar

JA Solar

Trina Solar

Canadian Solar

Hanwha Solutions

Risen Energy

First Solar

Chint Electrics

GCL System

SunPower

Solargiga

Shunfeng

EGing PV

Seraphim

Jinergy

LG Business Solutions

Jolywood

Tangshan Haitai

HT-SAAE

Talesun Solar

These companies compete on factors such as price, efficiency, durability, warranty, and after-sales service. The market has seen increasing consolidation as companies seek economies of scale and geographic expansion.

📥 Download Sample Report: Solar Photovoltaic (PV) Panels Market - View in Detailed Research Report

Future Outlook

The solar PV market is expected to continue its strong growth trajectory through the forecast period and beyond. Key trends to watch include:

Further Cost Reductions: Continued technological improvements and manufacturing scale will drive costs down further, making solar even more competitive.

Green Hydrogen Integration: Solar PV can power green hydrogen production, creating new synergies in the renewable energy ecosystem.

Floating Solar: Installing solar panels on water bodies is gaining popularity, especially in countries with land constraints.

Agrivoltaics: Combining solar energy generation with agriculture offers mutual benefits and land-use efficiency.

As the world continues to transition toward renewable energy, solar PV is expected to maintain its position as one of the fastest-growing energy sources. By 2032, solar is projected to become the largest source of electricity generation in many regions.

📥 Download Sample Report: Solar Photovoltaic (PV) Panels Market - View in Detailed Research Report

About Intel Market Research

Intel Market Research is a leading provider of strategic intelligence, offering actionable insights in energy, technology, and industrial sectors. Our research capabilities include:

Real-time market monitoring and analysis

Supply chain and manufacturing intelligence

Policy and regulatory impact analysis

Competitive benchmarking and strategy

Trusted by Fortune 500 companies, our insights empower decision-makers to drive innovation with confidence.

🌐 Website: https://www.intelmarketresearch.com

📞 International: +1 (332) 2424 294

Asia-Pacific: +91 9169164321

🔗 LinkedIn: Follow Us